Cecil Lee

Staff

-

Joined

-

Last visited

-

Yawn

-

-

-

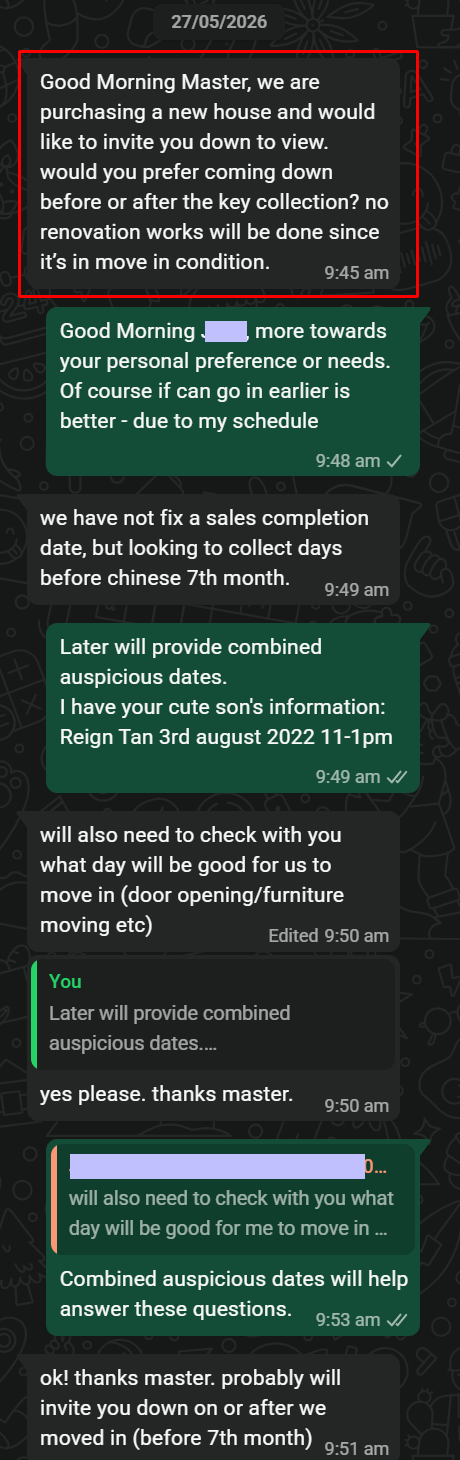

Good Morning Master, we are purchasing a new house and would like to invite you down to view. would you prefer coming down before or after the key collection? no renovation works will be done since it’s in move in condition

-

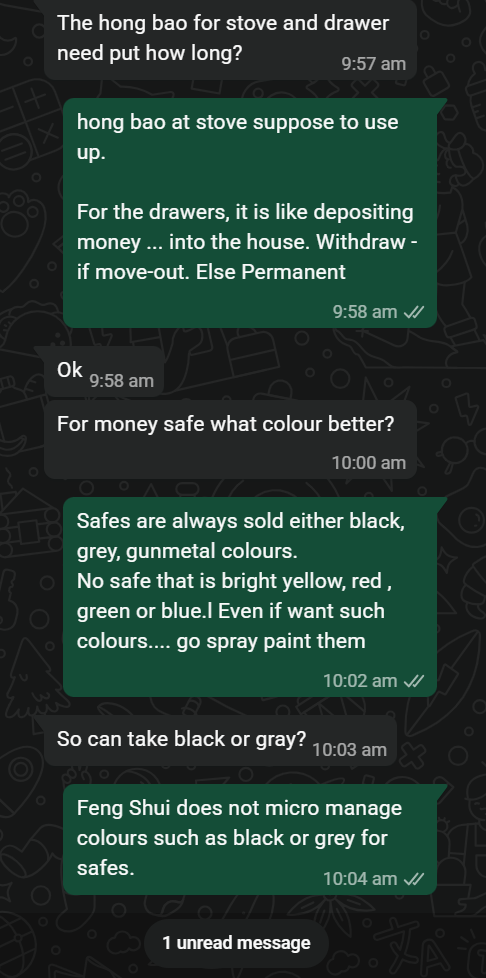

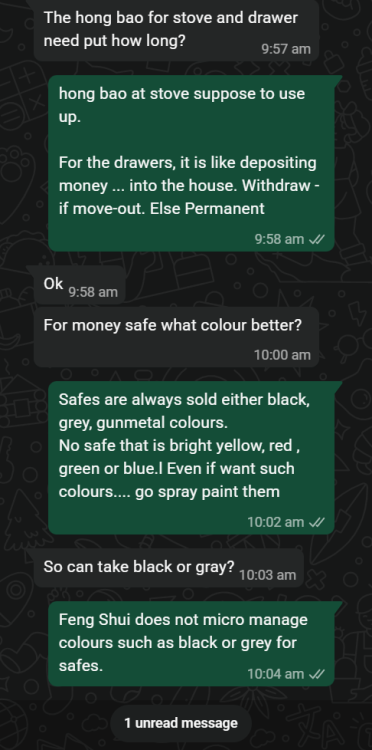

The hong bao for stove and drawer need put how long? hong bao at stove suppose to use up. For the drawers, it is like depositing money ... into the house. Withdraw - if move-out. Else Permanent

-

For money safe what colour better? Safes are always sold either black, grey, gunmetal colours. No safe that is bright yellow, red , green or blue.l Even if want such colours.... go spray paint them So can take black or gray? Feng Shui does not micro manage colours such as black or grey for safes.

-

-

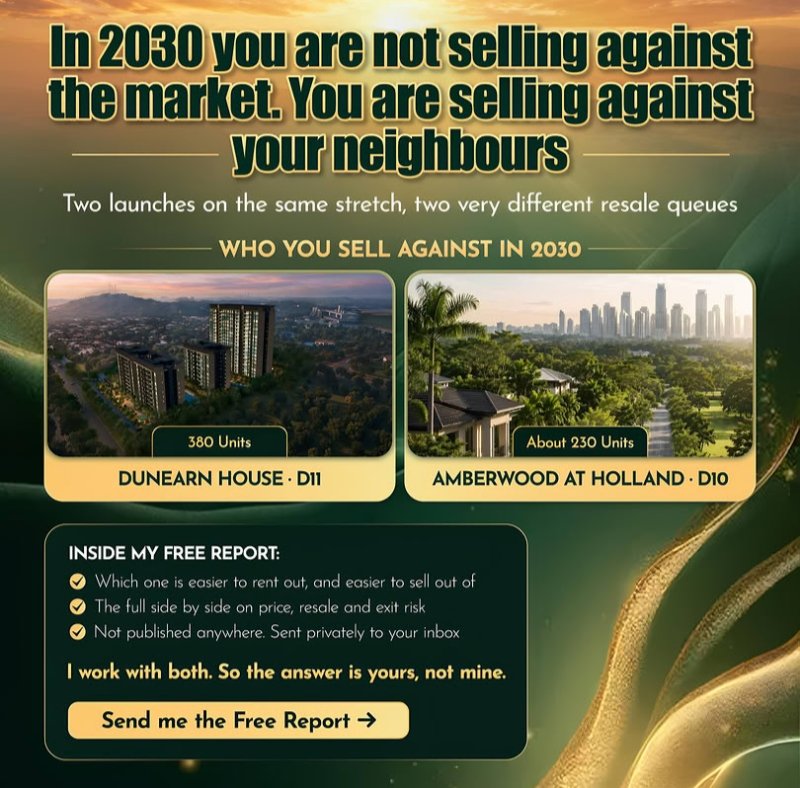

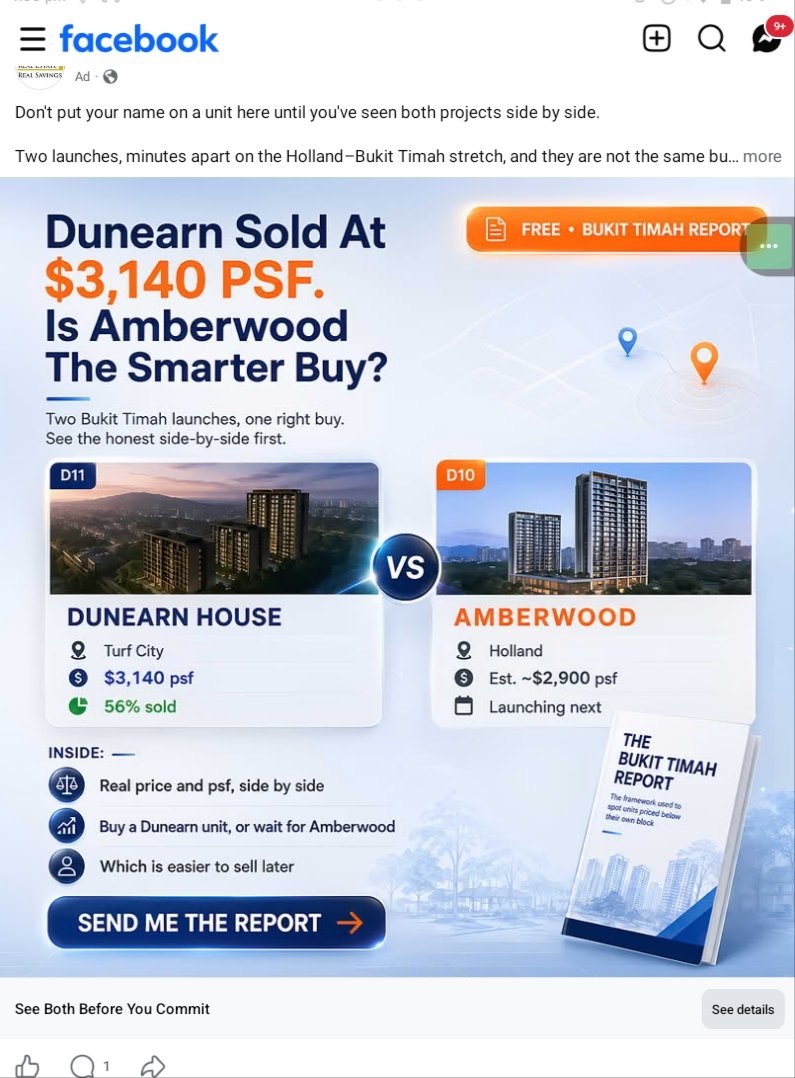

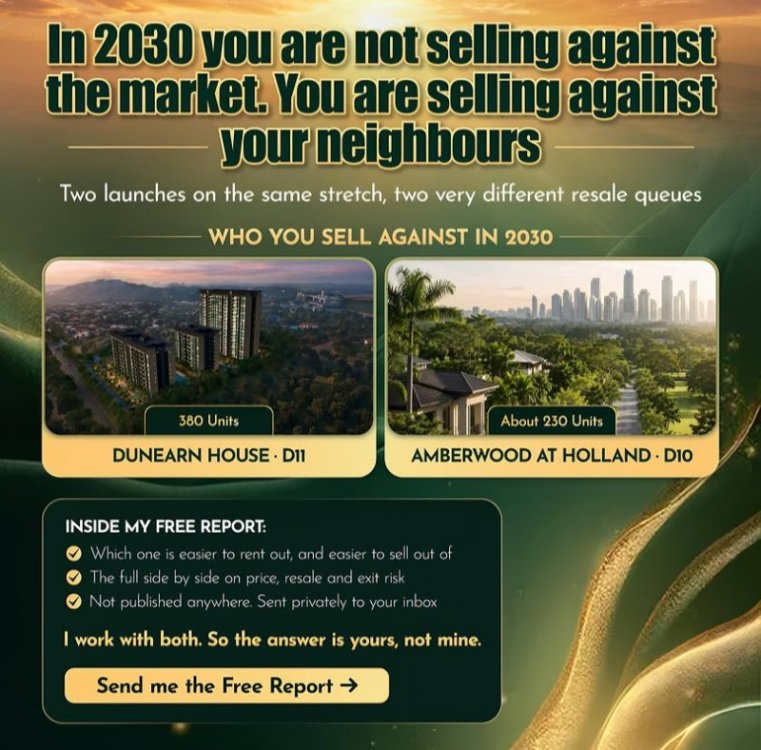

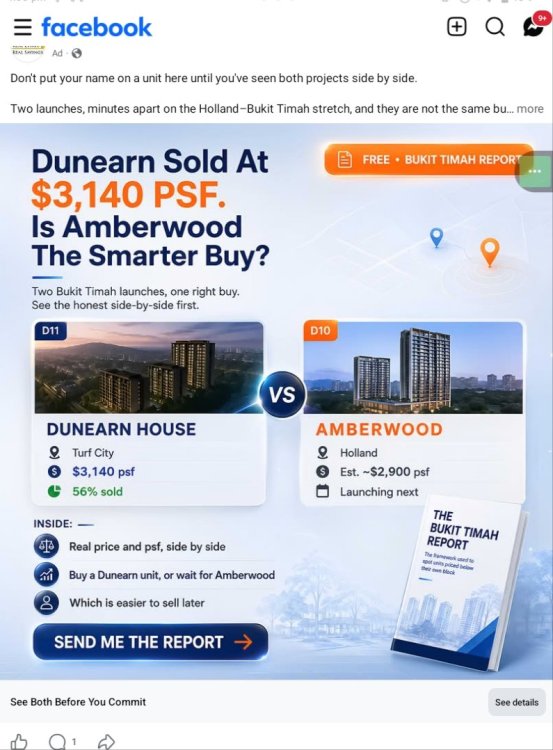

Dunearn House vs Amberwood?

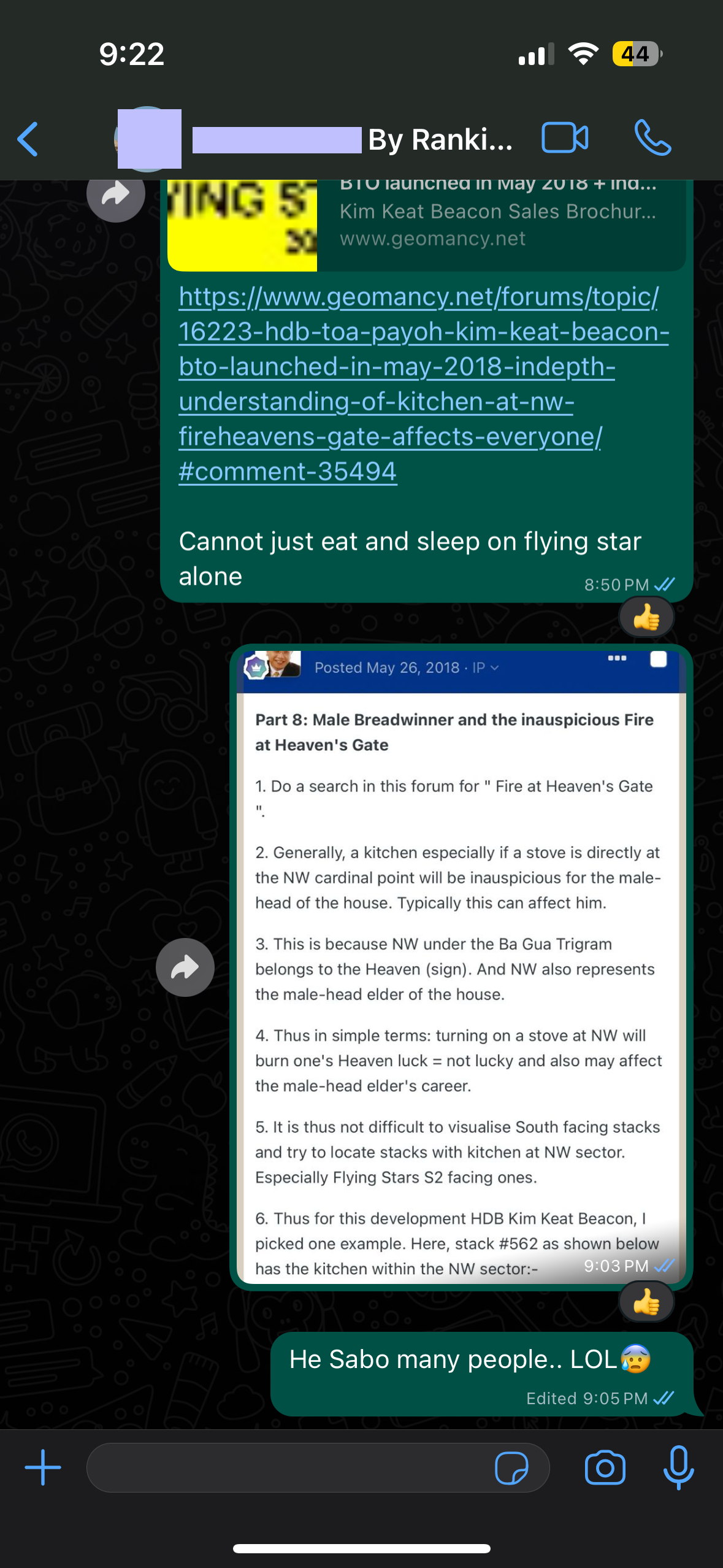

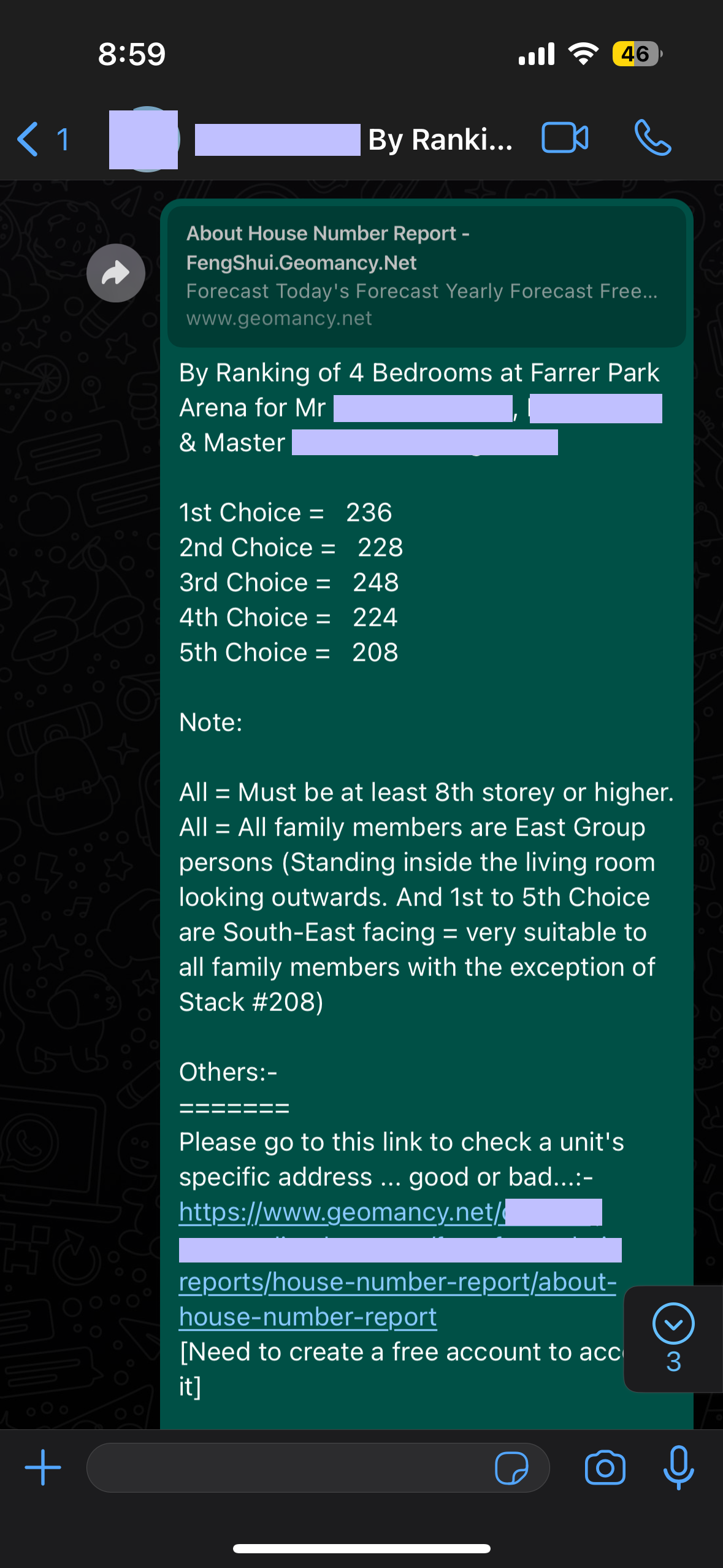

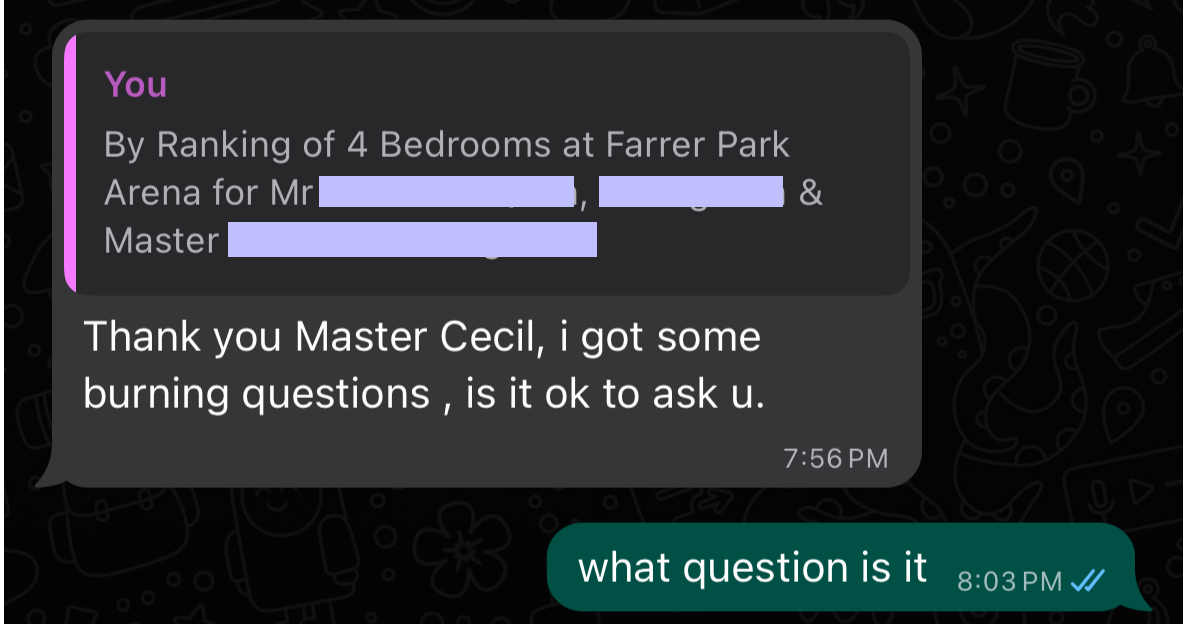

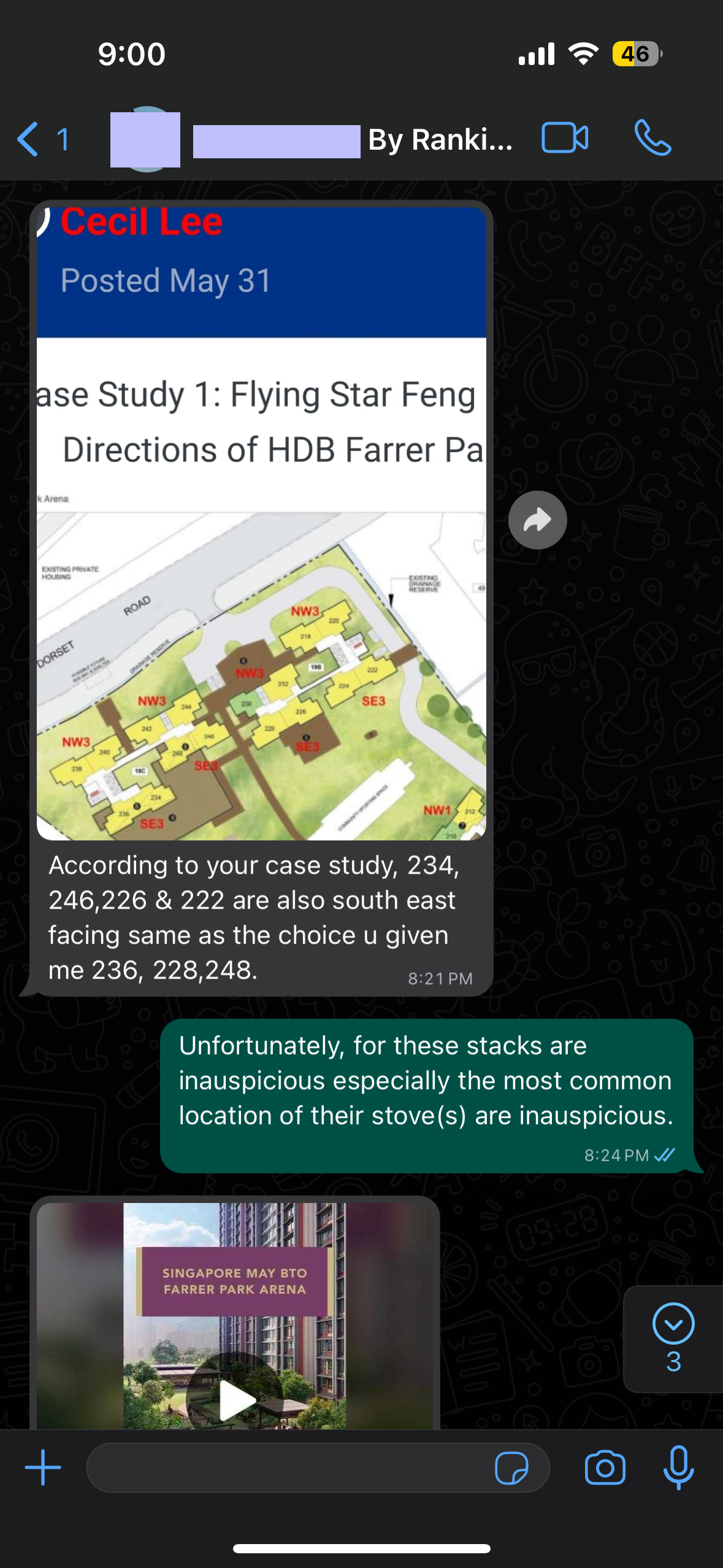

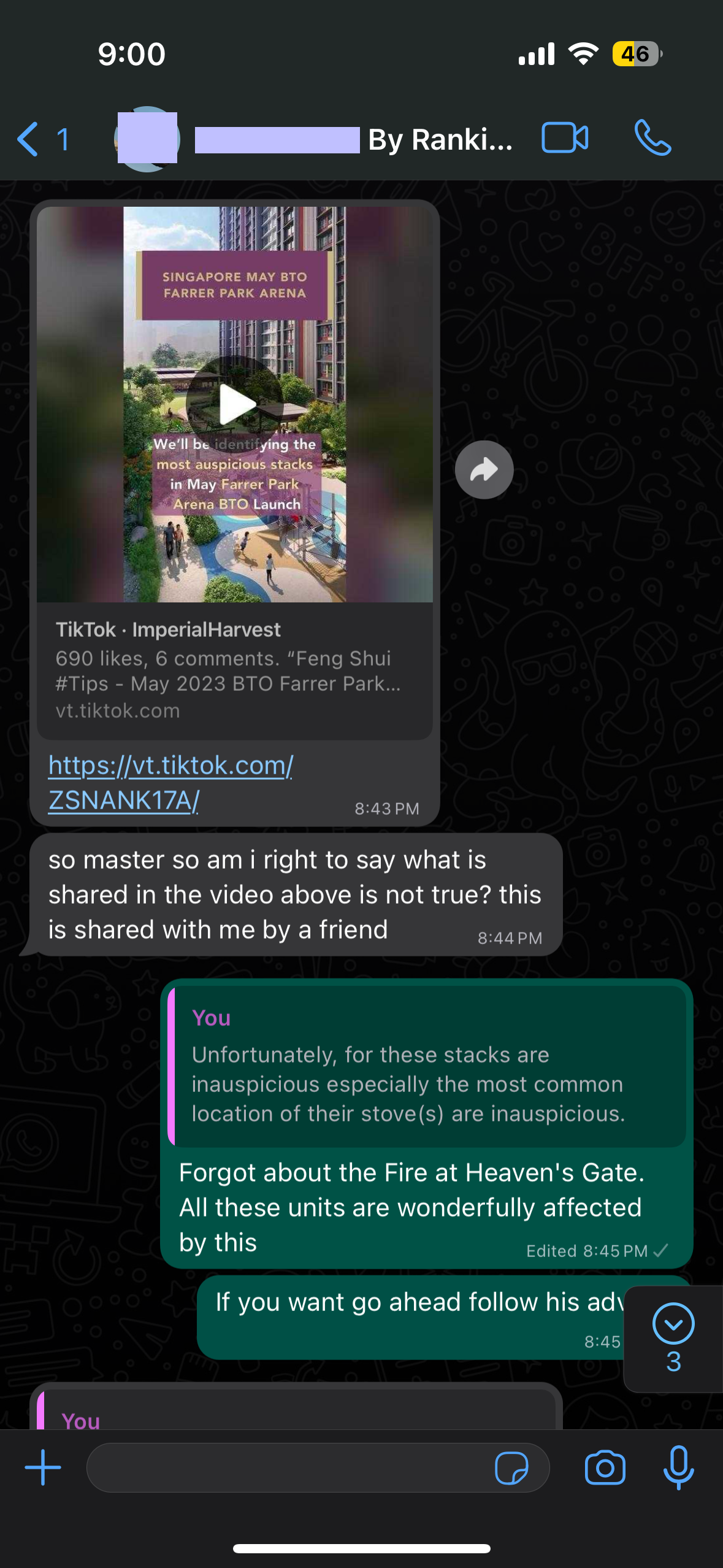

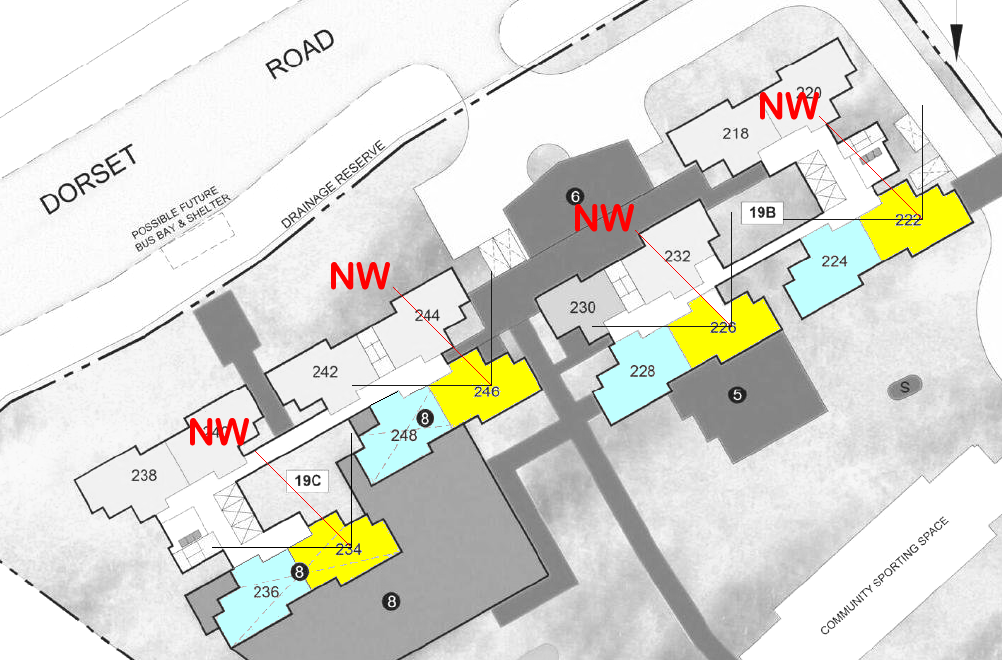

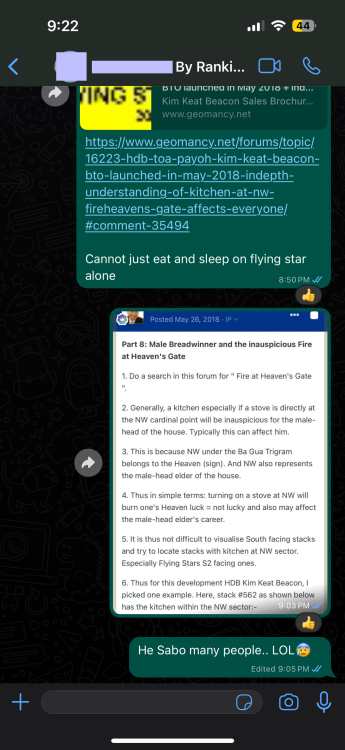

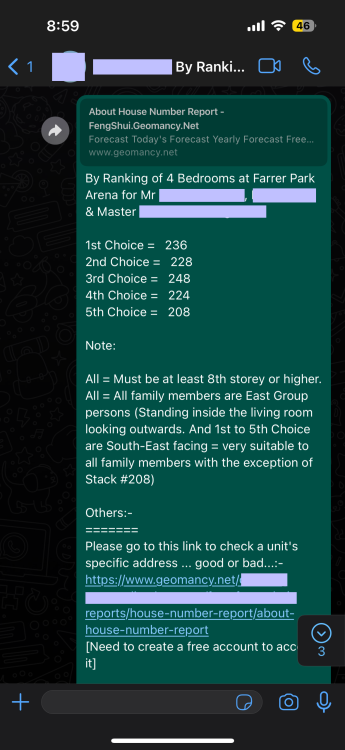

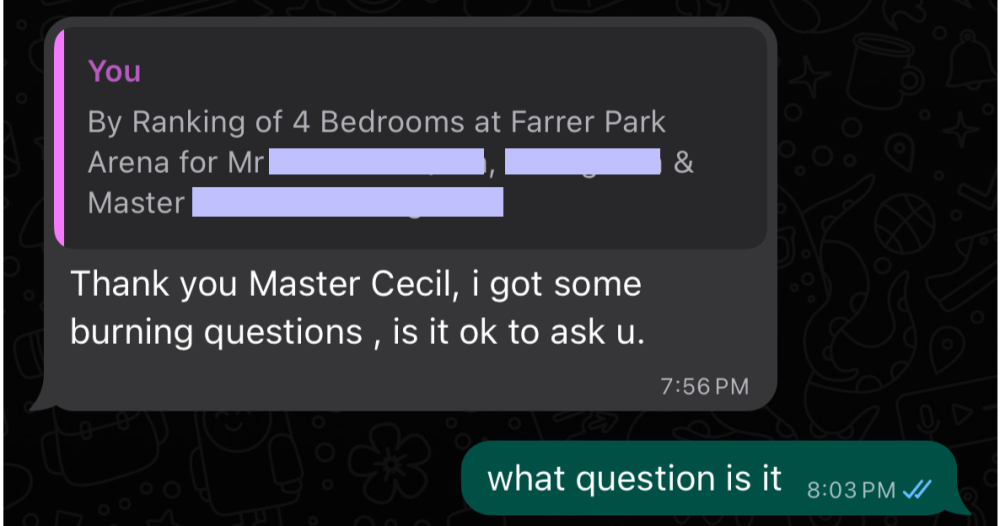

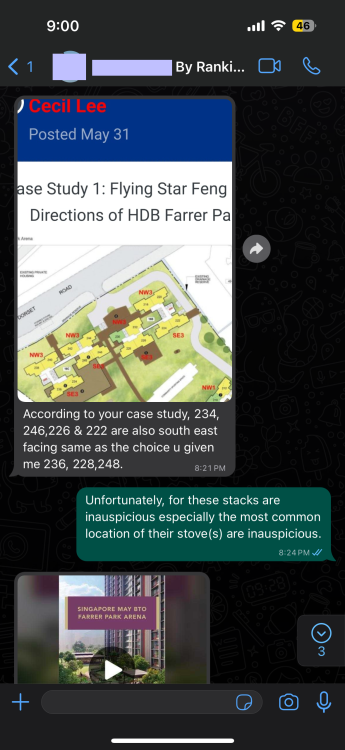

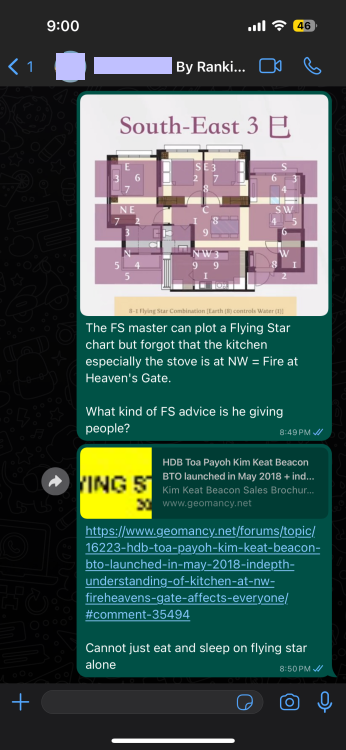

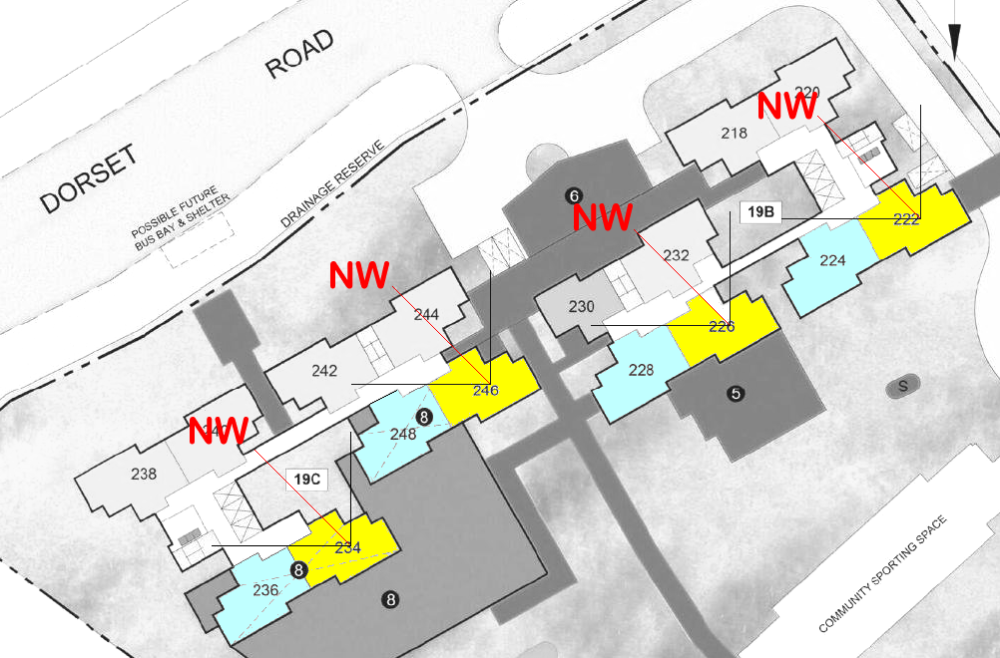

Why a Tik Tok Feng Shui Master’s Feng Shui Ranking Recommendation Can Be Wrong About this Case Study A client asked why my top-five HDB Farrer Park Arena stack rankings did not include stacks recommended in a TikTok by another Feng Shui Master. I explained I excluded those stacks because they have major Feng Shui flaws. Although stacks like #222, #226, #234, and #240 may look attractive and have similar facings to my top picks, their kitchen layout likely forces the stove into the NW sector (“Fire at Heaven’s Gate”), which is why they should be avoided. +++ Yellow Stacks #234, #246, #226, and #222 affected by unlucky Fire at Heaven's Gate +++ Case Study: Completed the ranking of 4 Bedrooms at Farrer Park Arena for the client on 31 October 2023 Client: Thank you Master Cecil, i got some burning questions, is it ok to ask u. Client: According to your case study, 234, 246, 226 & 222 are also south east facing same as the choice u given me 236, 228, 248 Client: "so master so am i right to say what is shared in the video above is not true? this is shared with me by a friend" (The client forwarded the TikTok video where the Feng Shui Master recommends stacks 234, 246, 226, and 222 as his choices, but I avoided these stacks. Why?) The Feng Shui master can plot a Flying Star chart but forgot that the kitchen especially the stove is at NW = Fire at Heaven's Gate. What kind of Feng Shui advice is he giving people? He Sabo many people.. LOL If the Feng Shui Master has done his homework properly, my client would not have any "burning" questions. LOL Did you buy any units in these stacks: 234, 246, 226, and 222, suggested by the Master in the "purple" TikTok video? Reference:

Why a Tik Tok Feng Shui Master’s Feng Shui Ranking Recommendation Can Be Wrong About this Case Study A client asked why my top-five HDB Farrer Park Arena stack rankings did not include stacks recommended in a TikTok by another Feng Shui Master. I explained I excluded those stacks because they have major Feng Shui flaws. Although stacks like #222, #226, #234, and #240 may look attractive and have similar facings to my top picks, their kitchen layout likely forces the stove into the NW sector (“Fire at Heaven’s Gate”), which is why they should be avoided. +++ Yellow Stacks #234, #246, #226, and #222 affected by unlucky Fire at Heaven's Gate +++ Case Study: Completed the ranking of 4 Bedrooms at Farrer Park Arena for the client on 31 October 2023 Client: Thank you Master Cecil, i got some burning questions, is it ok to ask u. Client: According to your case study, 234, 246, 226 & 222 are also south east facing same as the choice u given me 236, 228, 248 Client: "so master so am i right to say what is shared in the video above is not true? this is shared with me by a friend" (The client forwarded the TikTok video where the Feng Shui Master recommends stacks 234, 246, 226, and 222 as his choices, but I avoided these stacks. Why?) The Feng Shui master can plot a Flying Star chart but forgot that the kitchen especially the stove is at NW = Fire at Heaven's Gate. What kind of Feng Shui advice is he giving people? He Sabo many people.. LOL If the Feng Shui Master has done his homework properly, my client would not have any "burning" questions. LOL Did you buy any units in these stacks: 234, 246, 226, and 222, suggested by the Master in the "purple" TikTok video? Reference:

The truth about annual Feng Shui products: what’s sold as tradition has become a highly profitable buying trap. What many people don’t realize: annual Feng Shui products are less about balance and more about selling fear. Annual Feng Shui products aren’t guidance they’re a carefully engineered sales cycle. Let’s call it what it is: the annual Feng Shui buying cycle has become a commercialized scam. Understanding the Commercial Side of Modern Feng Shui The Annual Feng Shui Money Trap: Why You’re Told to Buy for All Nine Sectors Every Year The Feng Shui Sales Machine: How Annual “Cures” Turn Advice into Retail Annual Feng Shui Products Explained: Nine Sectors, Endless Purchases Separating Authentic Feng Shui from Product-Driven Practices Feng Shui Without Forced Buying: What Clients Are Rarely Told Many Feng Shui shops deliberately push customers to buy new items year after year, making it seem like these purchases are unavoidable. The bigger the family, the more objects we’re told we need, filling our homes with products we never truly needed in the first place. Over time, this becomes a repeating cycle—almost like an addiction—where people feel they have to make an annual pilgrimage to these so‑called Feng Shui masters. Fear, superstition, and guilt are quietly used to pressure people into buying again and again. In the end, the real purpose becomes clear: generating super‑normal profits for the sellers, while ordinary people unknowingly become their victims. Recognizing this pattern is the first step toward breaking free from it. Behind the friendly advice lies a clear motive: to push customers into buying as many products as possible—one for each of the nine sectors of their home. This isn’t guidance; it’s systematic upselling disguised as tradition. If we want this cycle to end, it starts with us. Please spread the word: when people stop buying out of fear, the selling stops too.

The truth about annual Feng Shui products: what’s sold as tradition has become a highly profitable buying trap. What many people don’t realize: annual Feng Shui products are less about balance and more about selling fear. Annual Feng Shui products aren’t guidance they’re a carefully engineered sales cycle. Let’s call it what it is: the annual Feng Shui buying cycle has become a commercialized scam. Understanding the Commercial Side of Modern Feng Shui The Annual Feng Shui Money Trap: Why You’re Told to Buy for All Nine Sectors Every Year The Feng Shui Sales Machine: How Annual “Cures” Turn Advice into Retail Annual Feng Shui Products Explained: Nine Sectors, Endless Purchases Separating Authentic Feng Shui from Product-Driven Practices Feng Shui Without Forced Buying: What Clients Are Rarely Told Many Feng Shui shops deliberately push customers to buy new items year after year, making it seem like these purchases are unavoidable. The bigger the family, the more objects we’re told we need, filling our homes with products we never truly needed in the first place. Over time, this becomes a repeating cycle—almost like an addiction—where people feel they have to make an annual pilgrimage to these so‑called Feng Shui masters. Fear, superstition, and guilt are quietly used to pressure people into buying again and again. In the end, the real purpose becomes clear: generating super‑normal profits for the sellers, while ordinary people unknowingly become their victims. Recognizing this pattern is the first step toward breaking free from it. Behind the friendly advice lies a clear motive: to push customers into buying as many products as possible—one for each of the nine sectors of their home. This isn’t guidance; it’s systematic upselling disguised as tradition. If we want this cycle to end, it starts with us. Please spread the word: when people stop buying out of fear, the selling stops too.

On 6th August 2026

On 6th August 2026

Change location of front door

Change location of front door

Hi, I've been reading your resources directory at resources.geomancy.net - it's one of the most comprehensive Chinese metaphysics link collections I've come across.

Hi, I've been reading your resources directory at resources.geomancy.net - it's one of the most comprehensive Chinese metaphysics link collections I've come across. Source & Credit:

Source & Credit: